So today I'm sick, my hands even hurt but my minds working well enough. The short story I want to share this for our kids. To offer help, but not in the "Here's a fish kind of help" but "Let me get you a fishing pole" kind of help.

Okay so follow along this journey if you want. I'll add VLOGS as we go (video blogs).

*Here is a link to my old You Tube Channel that has some advice on being resourceful.

How to get started.

1. Find your Why.

Why are you ready to change? Why do you want to learn how to get out of this darn mess. I was in a darn mess at age 33. $1400 negative a month (that's right). Shamefully buying groceries on my credit card. I was lost. I had been debt free just a few years before and we blew it. We weren't wild spenders we just didn't have the knowledge we needed. The bank gave us a big loan for a house we couldn't afford and it ate our lunch. I was sick and tired of being broke and scared. What's your why?

Video Lesson 1

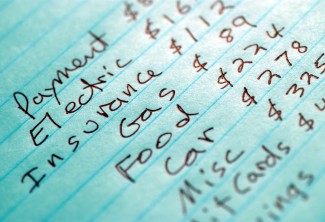

2. Write down all your bills and expenses (be honest) and your income (all of it). Make two columns.

First how much you make and when it comes in and total that monthly.

Example: Husband $950 every two weeks, Wife $1000 every 2 weeks. Random in our case. Total is $3950

Then all your bills, due date, how much: House note $1250, on the 5th.

If a bill is quarterly divide it by 4 and put it in your budget.

Just look at it and add up both columns. Subtract bills from income. This is what you have leftover.

Lesson 2 Video

3. Now look at what you can slash or get rid of NEEDS VS WANTS

You don't need expensive phone plans or cable. Those are wants.

Wants can be handled later. For now get busy getting out of debt.

Lesson 3 Video

4. Go on a spending freeze:

For the time being until you get an emergency fund make a budget for needs (food, basic transportation not joy riding) and all other spending gets frozen.

Lesson 4 Video

5. Save $1000 Emergency Fund

Get busy selling stuff. Yard Sales, Auctions, EBay, Craigslist, Resale Shops, Facebook Marketplace, old cars to the salvage yard. Clean up your crap and get rid of it (this also has a psychological impact on you in a positive way, you start to feel lighter). Get a $1000 fast. Then ear mark it for emergencies. Your tires are not an emergency you know you have that coming up, you will now start a savings account for those types of things.

Lesson 5 Video

6. Slash your budget and use excess money to pay debt. '

If you can slash your budget by $100 then you will put your $100 towards the smallest bill. Your goal will be to get debt paid off fast. I was a follower of this method long before Dave Ramsey was preaching this but he makes it really easy to understand. I know some people don't agree with his politics or religion or whatever but regardless just take the class and get the gist of it. It's the best program out there and it works.

Here is a link to the courses:

https://www.daveramsey.com/store/product/financial-peace-university-class#in-progress=1¢er=34.746481,-92.289595

7. I've already said it but I'm going to say it again. Sell everything you can and get out of debt.

YOU MAY NEED TO GET A SIDE HUSSEL, or as we old timers call it "a second job".

You can buy it again when you can pay for it. Get rid of the expensive cars, boats, phones, cable packages. I know many of you are upside down, figure out a way to get rid of all you can. You are going to have to study on how to do this. I actually sold the fancy house for $197,000 and moved into a fixer upper for $97,000 and lived there for 15 years. You heard me. We also got used cars, sold the boat and did the work ourselves on the house and it felt damn good to be out of debt.

At times in my life I've had two or three jobs (we actually still do until our farm is paid off). I've cleaned houses, taken in people's kids, dog sat, ran errands for money, worked a multitude of odd jobs. Right now I'm taking extra contracts and keeping my school open until I have a full years worth of living expenses paid up and our farm paid off.

One day I opened the door because my kid ordered a pizza (with money they earned) and a friend of mine was there delivering pizza (he was getting out of debt). This made me so happy!

Get your butt to work. As Dave says "There is a place for broke people, it's called work".

Lesson 6 & 7 video

8. Maintain this idea and hang with people who support you.

Find people who are living the same way. You will not be like the average person and they are everywhere and they are broke.

78% of Americans live pay check to pay check. You are going to be the 22%

Follow things on Instagram, Facebook, You Tube that have words like "frugal, debt free, simple living" In them. Find your people!

BE THE 22%. Link to article about 78% of Americans.

Here are some basics while you are getting out of debt and building your emergency fund up to six months.

- Meal plan and eat at home. Have a little fun money set aside and use coupons or find specials and share.

- Get rid of cable, rent movies from the library or get books. The library has tons of free resources and entertainment. FOR FREE! Well actually you pay taxes to use it, so do.

- Wear the clothes you have or buy your clothes at resale shops. If you must buy new then shop a sale but DO NOT SHOP for fun. I still buy 95% of all my clothes at resale.

- Pack your lunch. It's also a great way to lose weight.

- Work out at home, take a walk, use a free app, ride your bike. The library often has free yoga.

- You should not have one app on your phone that isn't free until you are out of debt.

- Stop shopping unless you need something.

- Tuesday nights are usually $5 movie nights in my town. I am not saying never have fun but find the deals and stick to the budget.

- For meals out find the cheap places to eat or go to lunch or use a coupon. Lunch is usually 1/2 the price of dinner and 1/2 the calories.

- Don't shop resale, garage sales, or flea markets for fun if you are getting out of debt or trying to build your savings. Only shop when you need something.

9. If the emergency fund gets used go back to filling it up then restart debt pay off.

10. Once the debt is done then focus on 3 months expenses in the bank.

If you make $4000 a month, then you will save $12,000.

Video 9 and 10

11. Pay off the mortgage and or invest in retirement.

Here is where Dave and I differ. And it depends. At this point you have

a. no debt

b. An emergency fund that has three to six months living expenses

Dave would say put 15% in retirement. It depends on your situation and how you feel about it. Right now I have a good amount saved and my husband has police retirement. I know that with no debt we will have more than what we make now. So I am choosing to pay off the mortgage first and then start putting more into my retirement. And that's not 100% true. I am self employed so each year I ask my accountant how much I should contribute to my IRA to save money and I usually add in about $4000.

I also am not super confident in our government right now and don't feel great about the stock market.

12. Invest in retirement and then you can contribute to your kids college fund or help them with college.

We have six kids. That's right. Three are currently in college and they get Pell Grants (some money not full), two of them get a load of scholarships and then they have to take out some loans. We pay what we can, this summer it was two summer tuition's which we paid cash for. We also pay for their car insurance and health insurance. We have also bought them all cars and we have helped at times but we also make them work for us if they need extra money. They are expected to work part time and go to college. I did and they can.

13. Help others or volunteer your time.

When you don't have to work or retire you can give your time to others or your money to programs and people who are less fortunate and that feels good. You may be able to help your kids go through college, or help a grand child. It feels good to give.

Video Lesson 11 through 13

I will be posting videos and updating this frequently.

* So as a side note I was on this journey 7 years ago when I got a divorce. That threw me into a state of living in poverty. Still I stayed out of debt, worked harder, paid all my bills, paid off my car and lived pretty well taking care of four kids on less than $45,000. a year. The first few years I made only $27,000 but had some child support. It was hard as heck. Now my husband (I got remarried in Jan.) and I have worked up to having a 40 acre farm (that is our only debt and we have quite a lot of equity as we paid for a lot of it as we built it). I have a decent retirement account, we have six months expenses put back and a savings for large bills that come up like house insurance or tires. Things can come up and surprises and I know life is not perfect but we try, surprises and emergencies are much easier to recover from when you have an emergency fund. If we have a slip we figure it out but we don't give up. We don't live a lavish lifestyle, we buy used items (often) from clothes to cars. We think about our purchases and we are now able to take a nice vacation (without any credit cards). Life is easier without debt and worry.